Earlier days, People would keep money in saving account. If they have lumpsum and want returns from that lumpsum, they would deposit then money in fixed deposit. Fixed deposit returns are 5.50 to 7.00% (annually) vary based on bank. It is all fine for 1980. In 1980, people want to keep the money in safest deposit and financial knowledge is not like today.

But in 21th century, India developed in financial front and best investment available in India for lumpsum investments such as mutual funds or PPF. PPF options for investor who does not want to risk. Mutual fund for all kinds of investors. They can choose debt mutual fund or equity mutual fund based on their financial knowledge and investment horizon.

Investment amount : 50000

Years : 5 years

Interest percentage: 6.5%

Interest earned : 18300.

Maturity amount : 18300 + 50000 = 68300.

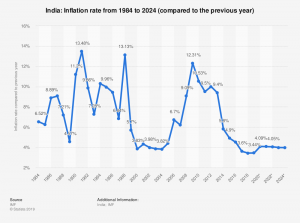

Average inflation rate in india is : 5.39 % . So after 5 years, your 65000 rupees is equal to 50000 rupees. Means that if you buy 20 gram gold at price of 50000 rupees in 2018, the same 20 gram gold would be 65000 in 2023. So final profit after inflation is,

Interest earned : 18300

Inflation : 15000 (-)

Profit earned : 3300.

Do you feel you money is grown in FD? Do you think it is good investment for you? It may be good for bank and not for investor.

Who people keep money in FD:

- People are satisfied with lower returns and fixed return even though it is low.

- Due to lack of financial knowledge of investment in India.

- Impact of financial knowledge transfer from your grandparents They think it is good, so they teach you same to you as well.

- Can avail load from FD in case of emergency. But interest would be calculated for loan. Usually the interest would be FD interest plus 1%. If personal loan against FD and cannot repay on time, you stand to lose your bank fixed deposit as the bank forecloses the fixed deposit to recover the money lent. This case you have to pay penalty to the bank as you withdraw money from bank before maturity.

Fixed deposit is not better investment against inflation rate.

Inflation history and Fixed deposit rates in India:

Better alternatives to FD:

There are plenty of options available to invest the lump-sum amount. Proper analysis and invest in mutual fund would increase the possibility of the returns.

If you want low risk, invest in liquid or debt mutual funds. But you investment for more than 5 years, you can select equity mutual funds. It would give best returns in long term. FD money would be locked and can’t be withdraw without penalty before maturity period. But mutual funds can be withdrawn whenever it is required. Since it is invested and managed by professionals, it would grow against inflation.

Bursting Mutual Fund Myths:

- Starting mutual fund is as easy as starting fixed deposit. It is hassle-free investment in India.

- Do not assume LIC, post office FD and SBI FD is only safest option for money. Even mutual funds are safest investment, it is monitored by SEBI. Do not think it is not safest, It is safest investment in bond mutual funds or liquidity mutual funds.

- Equity mutual funds give better return in long term. Investment cum saving. Your money grows by investing in stocks and bonds.

- You can view your investment report at any point of time and sell mutual fund at any point of time. No restriction and no hidden process.

Do your own analysis and park your money in mutual fund instead of fixed deposit. Fixed deposit is good for bank, mutual fund investment is good for you. Start investing..!! Start Mutual funds.!!!